Semiconductor & Robotics Industry Pulse

Price Momentum Builds Across MLCC, Memory, and Foundry; Robotics Captures Market Attention

Upstream Semiconductor Trends

- Winbond Signals Tight Supply Through 2027, Commits to Major Capacity Expansion

Winbond reported that its production capacity for 2026–2027 is already fully booked, with pricing expected to remain on an upward trajectory. The company approved a NT$42.1 billion investment for 2026 to expand customized DRAM, NOR Flash, and SLC NAND lines.

- Murata Weighs Price Increases for High‑End MLCCs Used in AI Servers

Murata’s chairman noted that the company is evaluating price adjustments for premium MLCCs required in AI servers, a segment where Murata commands roughly 70% market share.

- Jiejie Microelectronics Implements Multiple Rounds of Price Adjustments

Industry sources indicate that Jiejie Microelectronics issued several price‑increase notices in February, raising prices by 5%–20% across MOSFETs, thyristors, and optocouplers due to rising raw‑material costs.

- Hongwei Technology Raises Prices for IGBT and MOSFET Devices

Hongwei announced a ~10% price increase effective March 1, citing cost pressure from fluctuations in non‑ferrous metal prices.

- SMIC: Memory and BCD Processes in Short Supply, Prices Trending Up

SMIC confirmed that both memory and BCD foundry capacity remain tight, with pricing moving higher. Strong AI‑related memory demand is crowding out supply for smartphones and other mid‑/low‑end applications.

- TSMC to Shift Majority of 8‑Inch Capacity to VIS

Reports suggest TSMC will gradually transfer up to 80% of its 8‑inch wafer output to VIS through order migration, equipment relocation, and technology collaboration, allowing TSMC to reallocate resources toward AI‑driven advanced processes.

- Samsung Accelerates Construction Timeline for Pyeongtaek P5 Fab

Samsung has reportedly instructed contractors to begin early cleanroom work for the P5 fab by 2Q26—six months ahead of schedule. The facility is positioned as a next‑generation production hub for HBM and other AI‑focused products, with operations targeted for 2028.

- ADI Posts Strong FY26 Q1 Results

Analog Devices reported USD 3.16 billion in revenue for Q1 FY26, up 30% YoY, with operating profit more than doubling. Growth was driven by industrial and communications markets.

- Western Digital Plans Partial Divestment of SanDisk Stake

Western Digital announced plans to raise USD 3.09 billion by selling part of its stake in SanDisk, the flash‑memory subsidiary it spun off last year.

Robotics & Downstream Applications

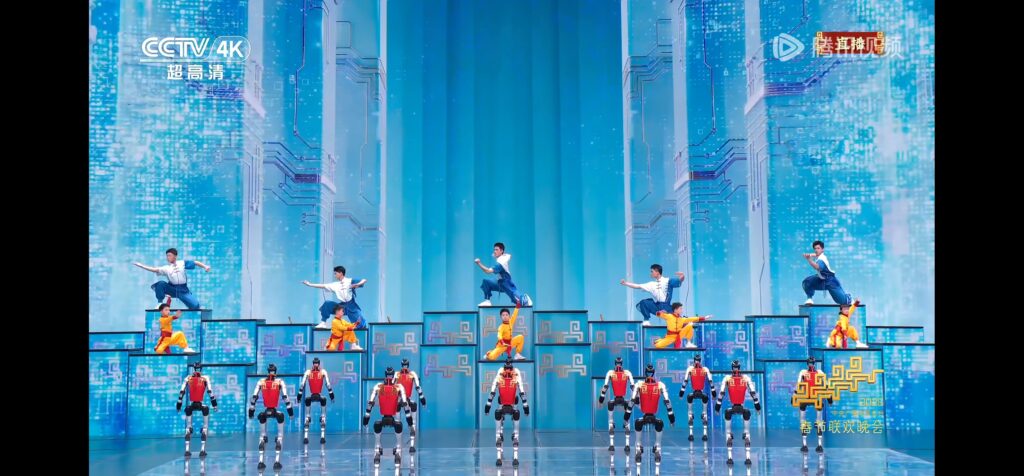

- Four Chinese Humanoid‑Robot Companies Featured on 2026 CCTV Spring Festival Gala

Unitree, Songyan Dynamics, Magic Atom, and Galaxy General showcased humanoid robots across multiple performance segments, highlighting rapid progress in domestic supply‑chain maturity and localization of core components.

- Spring Festival Exposure Sparks Market Optimism

Analysts note that the Gala appearance significantly broadened public awareness of humanoid robots, accelerating commercialization and attracting capital inflows. With Tesla’s Gen3 announcement approaching, the sector is expected to see further catalysts.

- Unitree Targets 10,000–20,000 Humanoid‑Robot Shipments in 2026

Founder Wang Xingxing highlighted breakthroughs in autonomous cluster‑control technology, enabling rapid multi‑robot formation running at up to 4 m/s. He expects global humanoid‑robot shipments to reach several tens of thousands this year, though progress remains constrained by embodied‑AI limitations.

- Acer: PC Market to See Lower Volume but Higher ASP

Acer’s chairman expects PC shipments to decline 6%–9% in 2026, while average selling prices rise by double digits due to upstream cost pressure. January shipments surged 40% YoY as customers pulled in orders ahead of anticipated price increases.

- Europe’s Memory Shortage Fuels Surge in Refurbished PC Sales

The UK’s refurbished‑PC market doubled YoY in 4Q25, surpassing Germany, as memory shortages and rising prices pushed buyers toward cost‑effective alternatives.

Industry Partnerships & Strategic Moves

- STMicroelectronics Signs Multi‑Billion‑Dollar Agreement with AWS

ST will supply high‑performance mixed‑signal solutions, advanced microcontrollers, and energy‑efficient analog/power ICs to support hyperscale data‑center infrastructure.

- Renesas and GlobalFoundries Deepen Collaboration

Renesas will gain expanded access to GF’s specialty processes—including FDX FD‑SOI, BCD, SiC, and MOS+NVM—with tape‑outs expected to begin mid‑2026.

Market Data & Outlook

- SEMI: Silicon‑Wafer Shipments to Rebound in 2025

Global wafer shipments are projected to grow 5.8% to 12,973 MSI, driven by AI‑related demand for epitaxial and polished wafers. Revenue, however, is expected to decline 1.2% due to weak traditional‑semiconductor demand and pricing pressure.

- Omdia: DDIC Market to Dip Slightly in 2025, Stabilize in 2026

LCD‑TV DDIC demand is expected to fall 9%, while monitors, notebooks, and automotive displays show positive momentum. AMOLED and smartwatch DDIC demand will see only modest growth.

- TrendForce: Smartphone Production to Drop 10% in 2026

High memory prices are pushing smartphone BOM costs sharply higher, with memory now accounting for 30%–40% of total cost. In a pessimistic scenario, production could fall by 15%.

- Korea Customs: Chip Exports Surge 134% in Early February

Korea’s export data shows strong semiconductor momentum, with chips up 134% and computer peripherals up 129%, offsetting declines in automotive exports.